European Dependence to a Rotating Market Portfolio: What 20 Years of Maldives Arrivals Reveal

29 May 2026, 06:48 · by i.zuhuree

The Maldives tourism story has often been told through one dominant market at a time. But I argue that the deeper pattern in the arrivals data is more interesting: the Maldives has not simply replaced one market with another. It has become a more diversified, more volatile, and more strategically demanding source-market portfolio.

For many years, the traditional European markets carried the industry. Then China became the single most visible growth story. After the pandemic, India and Russia briefly reshaped the rankings, before China returned to the top in 2024.

This matters because source markets are not just numbers in an arrivals table. They affect air access, seasonality, room pricing, food and service expectations, resort sales channels, guesthouse demand, transfer systems, language needs, and marketing budgets. For policymakers, destination marketers, hotel operators, and investors, the question is no longer “which country is number one?” The better question is: how resilient is the Maldives source-market mix, and what does each market contribute to the tourism model?

How I Read the Data

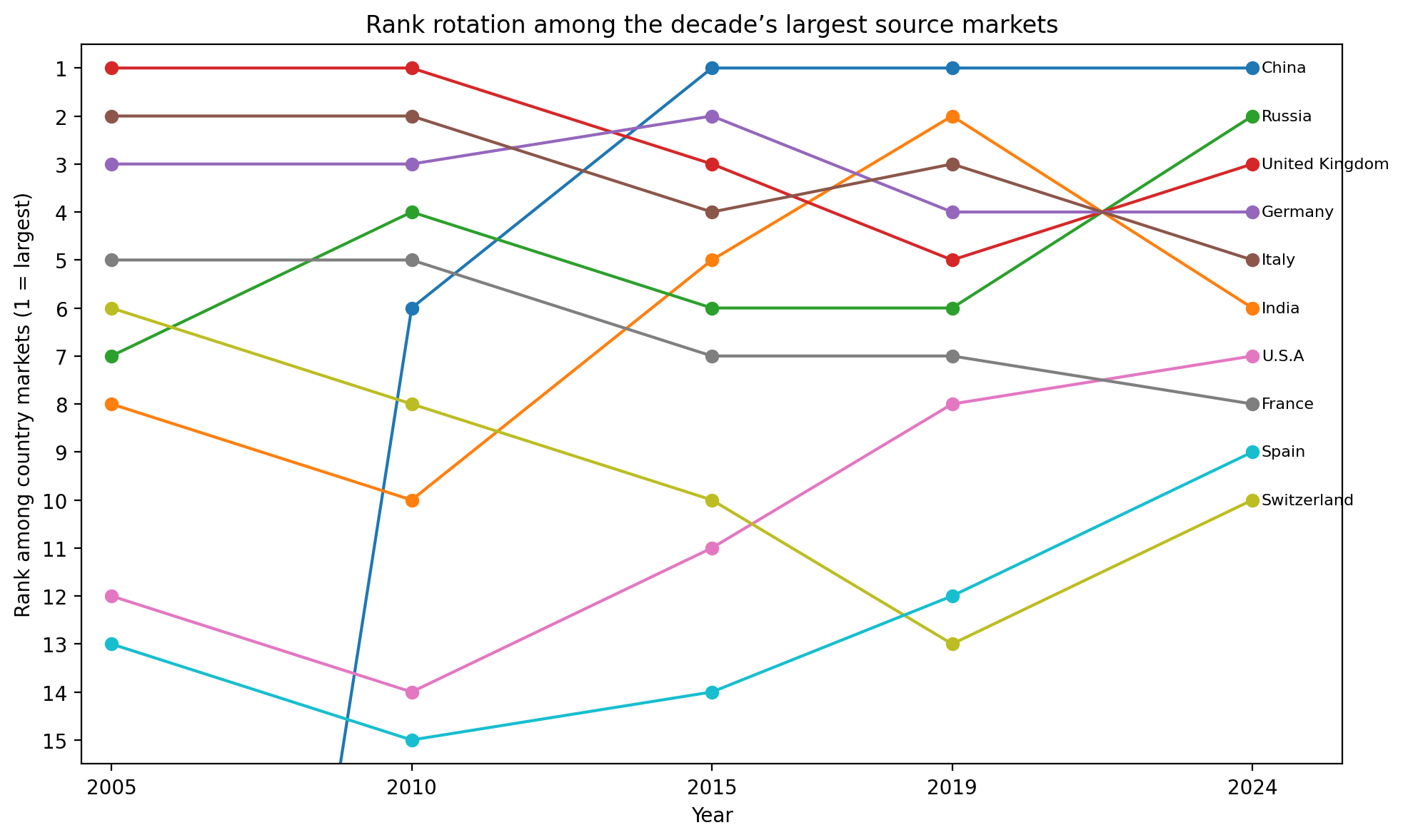

I analysed annual tourist arrivals by source country , focusing on country rows rather than regional or aggregate “other” rows. I used two main windows: the past 20 years, defined as 2005–2024, and the past 10 years, defined as 2015–2024. For each period, I ranked markets by cumulative arrivals, then compared their positions in selected years: 2005, 2010, 2015, 2019, and 2024.

The analysis is descriptive, not causal. The arrivals data shows what happened; it does not directly prove why it happened. Therefore, when I discuss data, I treat them as evidence-based interpretations rather than definitive causal estimates.

The Maldives Has Moved from Dominance to Portfolio Risk

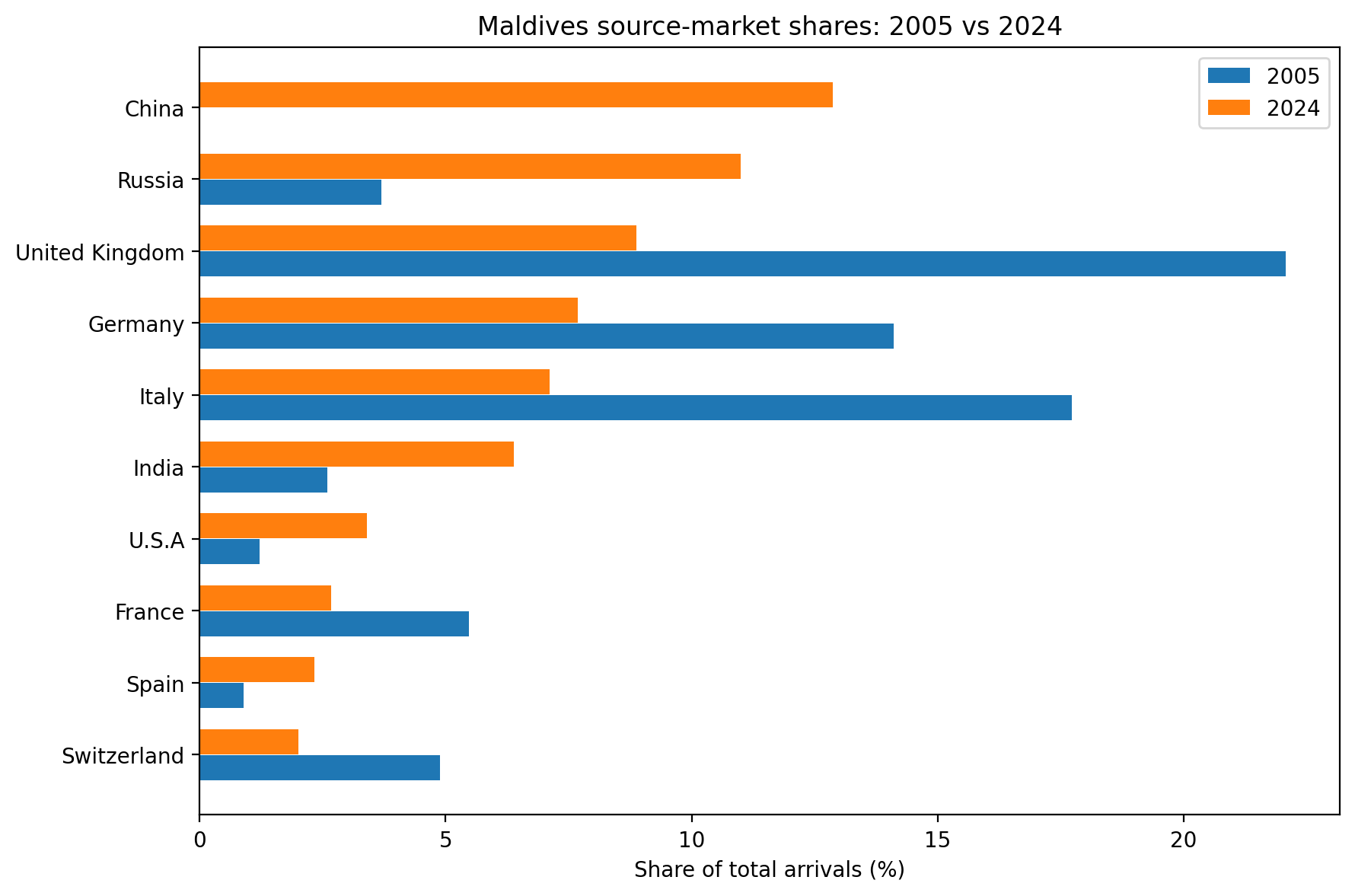

In 2005, the Maldives was still heavily shaped by European demand. The United Kingdom, Italy, and Germany alone accounted for 53.9% of total arrivals that year. The top ten country markets accounted for 80.6% of all arrivals. This was a highly concentrated tourism structure: strong, but exposed.

By 2024, the picture had changed. China was again the largest market, with 263,340 arrivals and a 12.9% share. Russia followed with 225,204 arrivals and an 11.0% share. The United Kingdom, Germany, Italy, India, the United States, France, Spain, and Switzerland completed the top ten. The top ten still mattered enormously, but their combined share had fallen to 64.4%. That is a major structural change. The Maldives still depends on large markets, but it is no longer as dependent on a narrow European core or on one Asian market.

The 20-year cumulative ranking captures the long arc. From 2005 to 2024, China generated 3.22 million arrivals, the largest total among all country markets. The United Kingdom followed with 2.20 million, Germany with 1.90 million, Italy with 1.77 million, Russia with 1.68 million, and India with 1.61 million. These six markets together tell the whole transition: Europe remained important, China became transformational, and Russia and India became central to the post-pandemic structure.

The 10-Year View: China Leads, But the Post-Pandemic Engine Is Broader

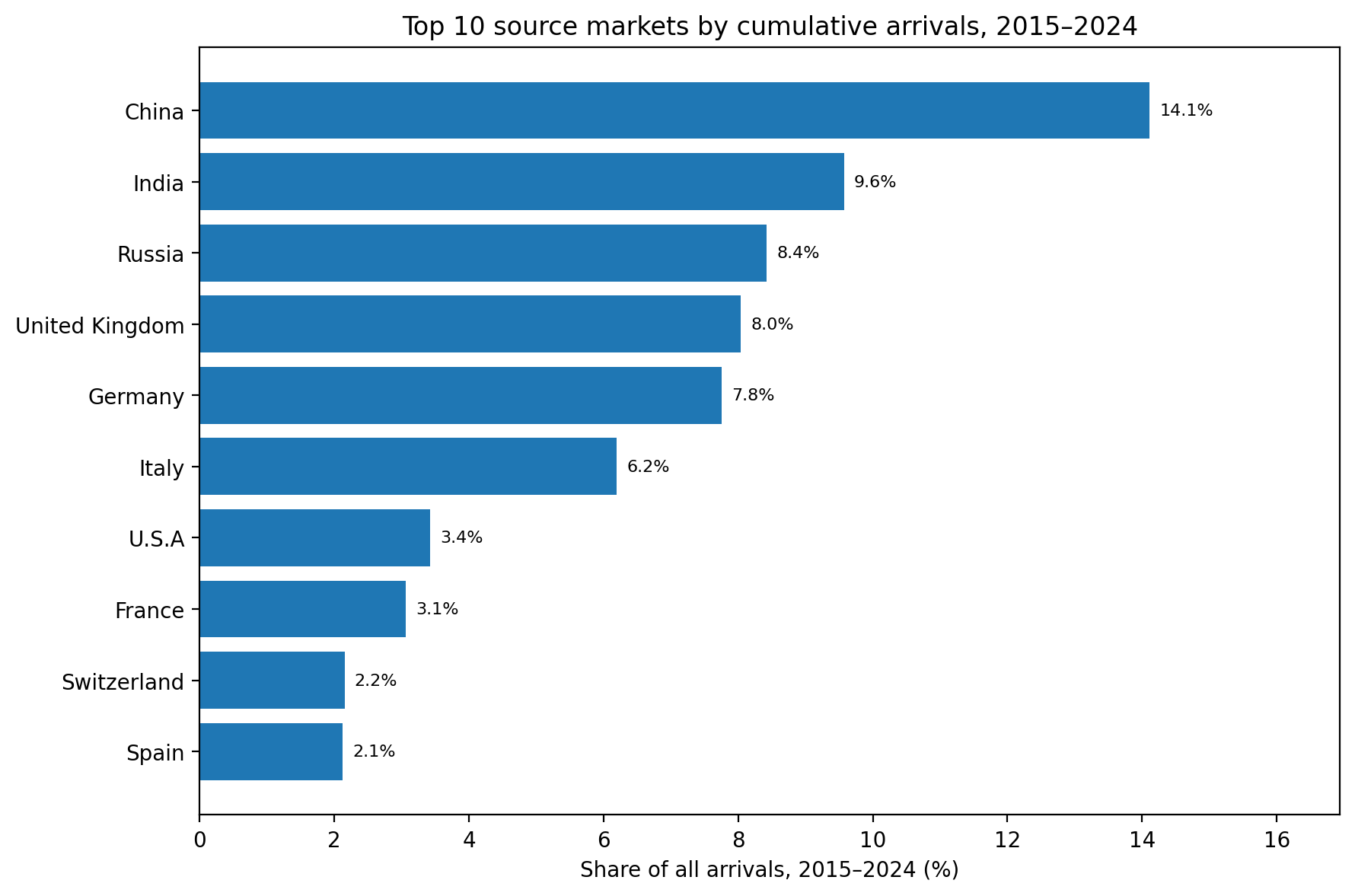

The past decade gives a sharper view of recent strategy. Between 2015 and 2024, China remained the largest cumulative market with 2.06 million arrivals. India came second with 1.39 million, Russia third with 1.23 million, followed by the United Kingdom, Germany, Italy, the United States, France, Switzerland, and Spain.

The decade ranking is important because it shows that the Maldives’ current demand base is no longer just traditional Europe plus China. India and Russia now sit ahead of the United Kingdom, Germany, and Italy in cumulative arrivals over the last ten years. The United States also moved into the decade top ten, which is notable given its distance from the Maldives.

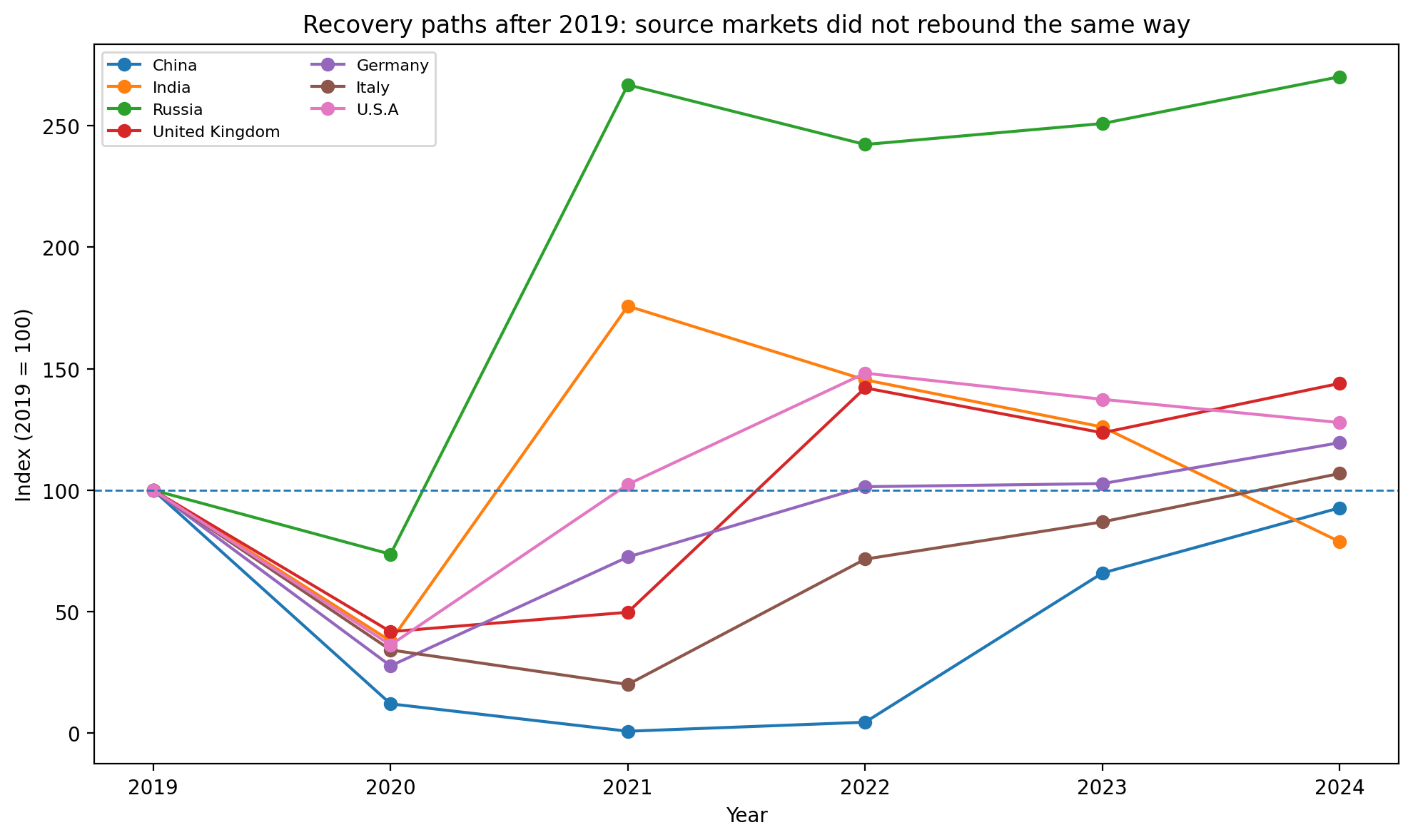

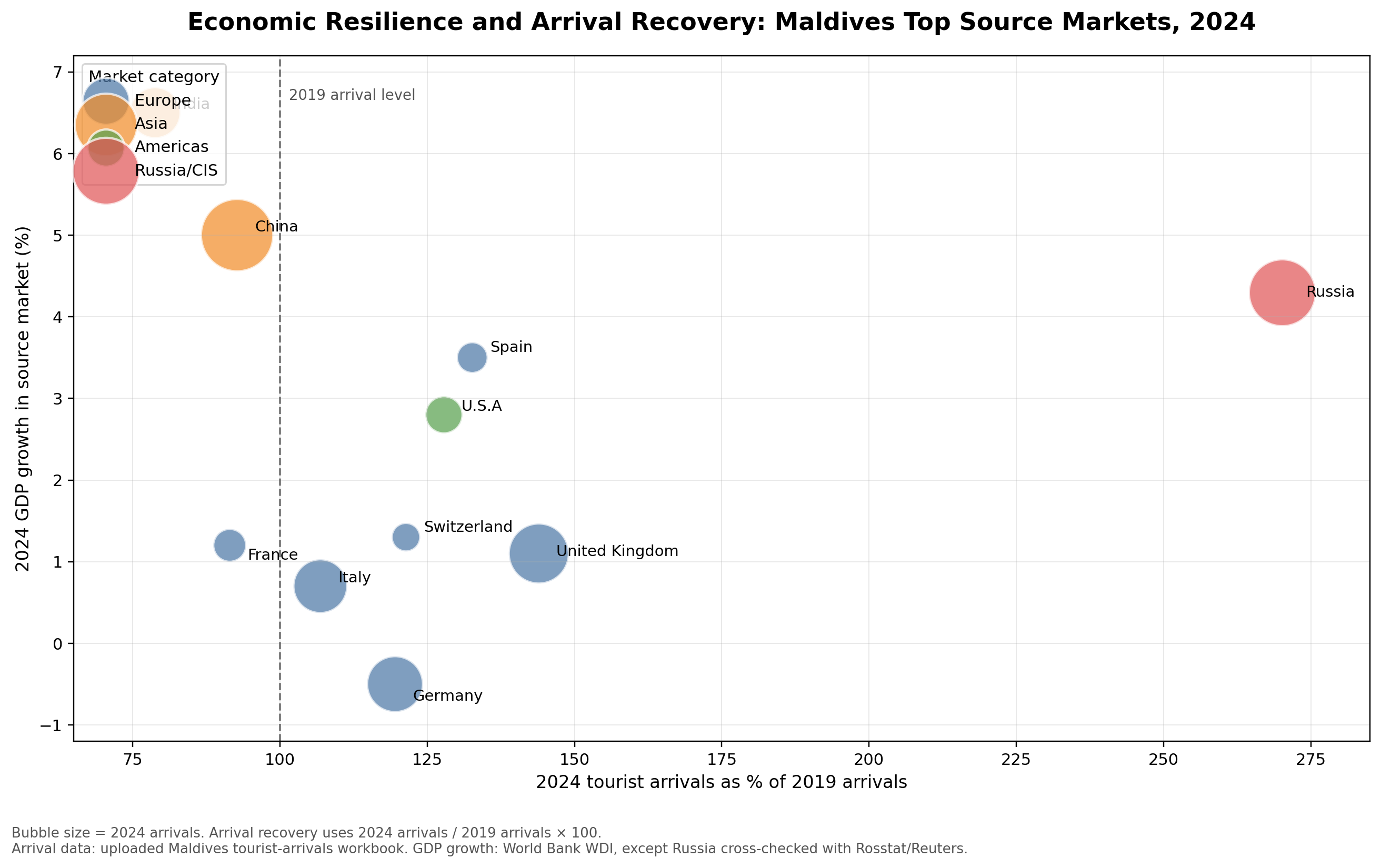

The Figure below shows Post-Pandemic recovery paths of Maldives’ key source markets after 2019. Using 2019 as the baseline index of 100, Russia became the strongest outlier, rising to about 270% of its pre-pandemic level by 2024. India surged early, reaching around 175% in 2021, but then declined sharply to about 79% by 2024, thus its recovery-period spike was not sustained. China, once the largest pre-pandemic market, collapsed during 2020–2022 but recovered to about 93% of its 2019 level by 2024. Traditional markets recovered more steadily: the UK reached about 145%, Germany 120%, Italy 107%, and the U.S. 128% by 2024.

This is where the industry story becomes practical. China still matters, but it no longer explains the whole growth model. India matters for regional demand and rapid shock recovery. Russia matters because it has become one of the strongest post-pandemic performers. Europe matters because it remains the dependable base. The United States matters because long-haul premium demand is becoming more visible.

Demand-Side Story is Not Typical: Macroeconomics, Shocks, and Uneven Recovery

The demand-side story is not simply that some countries like the Maldives more than others. It is also a story about if macroeconomic conditions, travel restrictions, household confidence, exchange rates, inflation, and outbound travel behaviour interacted with the Maldives’ own tourism product.

China is the clearest example. In the arrivals dataset, China returned to first place in 2024 with 263,340 arrivals, but it remained below its 2019 level of 284,029. This is important. China’s economy still grew in 2024, but outbound travel did not fully behave like the pre-pandemic Chinese market. Reports on Chinese outbound tourism in 2024 pointed to higher travel costs, visa frictions, a weaker yuan, property-market pressures, youth unemployment, and a stronger preference for domestic and short-haul travel. This means the Maldives should not treat China’s return to number one as a simple restoration of the old market. It is a recovered market, but not yet the same market.

India tells the opposite story. India was one of the Maldives’ strongest recovery markets in 2021, reaching 291,787 arrivals, but by 2024 arrivals had fallen to 130,805. That decline is striking because India’s macroeconomic conditions were not weak; India recorded strong GDP growth in 2024. Therefore, the fall in Indian arrivals cannot be explained by economic slowdown. It is more likely that the 2021–2022 surge reflected proximity, open routes, pent-up travel demand, and the fact that India was one of the fastest markets to reconnect after the pandemic. By 2024, that recovery premium had faded. Political sentiment, pricing, competing destinations, and market positioning may also have mattered.

Russia is the most unusual recovery story. Russian arrivals reached 225,204 in 2024, compared with only 83,369 in 2019. That means the Russian market was more than two and a half times its pre-pandemic size. This should not be read simply as evidence of broad Russian consumer strength. Russia’s economy grew in 2024, but it also faced high inflation, sanctions, currency pressures, and war-related distortions. The more plausible interpretation is that the Maldives captured a resilient high-income outbound segment, helped by accessibility, destination substitution, and the appeal of a luxury beach destination outside the usual European travel circuit.

The traditional European markets show a different pattern. The United Kingdom, Germany, and Italy all exceeded their 2019 arrivals by 2024, even though European macroeconomic conditions were not especially strong. Germany’s economy contracted in 2024, while the UK and Italy recorded low growth. Yet UK arrivals rose from 126,199 in 2019 to 181,644 in 2024; Germany rose from 131,561 to 157,246; and Italy rose from 136,343 to 145,672. This suggests that mature European demand for the Maldives is relatively resilient. These markets may not grow explosively, but they remain valuable because of repeat visitation, tour-operator familiarity, winter-sun demand, established air links, and a high-income traveller base.

The United States is also worth noting. US arrivals increased from 54,474 in 2019 to 69,620 in 2024. Given the distance, this growth is significant. It suggests that the Maldives is becoming more visible as a long-haul premium destination for American travellers. The US economy performed relatively strongly in 2024, which is consistent with the growth in high-value long-haul travel. For the Maldives, the US should not be viewed as a volume market like China or India, but as a potential value market.

The demand-side conclusion is therefore more nuanced. China remains essential, but its recovery is still incomplete. India’s fall shows that macro growth alone does not guarantee arrivals. Russia’s surge shows how geopolitical and substitution effects can reshape demand. Europe shows the value of mature, resilient, high-income markets. The United States shows the possibility of long-haul premium growth. For destination strategy, this means Maldives should not chase arrivals blindly. It should classify markets by economic resilience, connectivity, spending potential, seasonality, and vulnerability to shocks.

Supply Side Story: The Product Became Broad Enough to Absorb New Markets

The supply-side interpretation is also important. The Maldives did not receive more diverse markets simply because global demand changed. The product itself also changed. The traditional resort model remained central, but the broader accommodation mix expanded, especially through guesthouses and local-island tourism. As I have argued in an earlier post, By 2024, official accommodation data showed a large and varied tourism supply base: resort beds remained dominant, but guesthouse beds formed a significant part of registered capacity. This matters because different markets do not consume the Maldives in the same way. Some are drawn mainly to luxury resorts and private-island experiences. Others are more price-sensitive, more regionally connected, or more open to guesthouses, local islands, and shorter stays.

The arrival data alone cannot tell us which nationalities stayed in resorts, guesthouses, hotels, or safari vessels. That is a limitation. But the market pattern strongly suggests that the Maldives is no longer serving a single type of tourist through a single product model. A more diverse source-market base requires a more differentiated tourism product: ultra-luxury resorts, family resorts, mid-market islands, guesthouses, dive products, wellness products, and short-break regional packages.

What This Means for the Industry

For policymakers, the first lesson is that market diversification should be treated as risk management, not as a slogan. The 2015 China peak and the 2021 India-Russia recovery both show how quickly the market structure can change. Maldives tourism policy should track concentration risk, not just total arrivals. For destination marketers, the lesson is segmentation. Europe should be managed as a mature but valuable base. China should be rebuilt carefully, without assuming the 2015 structure will automatically return. India needs a more refined strategy because the post-pandemic surge was not fully sustained into 2024. Russia needs continued attention, but also risk monitoring.

The United States deserves a premium long-haul strategy, especially for high-value segments. For hotel operators, the data suggests that market agility is now an operational capability. Language skills, cuisine, payment systems, sales channels, family facilities, wellness offers, and activity design may need to match changing source-market composition. A resort or guesthouse that depends on one market is exposed.

For investors, the key point is that capacity should be matched to market behaviour. More beds alone are not a strategy. The right question is: which market, which product, which season, which price point, and which air-access pathway?

Building a Portfolio, Not Chasing a Winner

The strongest lesson from the data is that Maldives tourism stakeholders should stop thinking in terms of a single winning market. In 2005, the industry leaned heavily on Europe. In 2015, China looked like the future. In 2021, India and Russia carried recovery. In 2024, China returned to number one, but Russia, the United Kingdom, Germany, Italy, India, and the United States all mattered. Rank rotation show that since 2010 the U.S. and Spain increased rank by 7 points and 5 points, respectively, which may require a separate investigation. One area that may warrant broader analysis is the impact of marketing efforts in these countries.

That is the new reality. The Maldives is now a portfolio destination. Its strength will depend not only on attracting more tourists, but on balancing markets with different income profiles, travel behaviours, connectivity needs, seasonality patterns, and product expectations. The next phase of Maldives tourism strategy should therefore be built around market balance, route intelligence, product differentiation, and better data linking arrivals to spending, accommodation type, length of stay, and environmental impact.

The story in the arrivals data is clear: the Maldives has become more global, but also more exposed to market rotation. The opportunity is to manage that rotation deliberately rather than react to it after each shock.